How golf betting margins have changed over the years

How the gambling market has changed: a history of bookmaker overrounds

If you've ever placed a golf bet and wondered why the bookmaker always seems to come out on top, the answer lies in a concept called the overround — the built-in profit margin baked into every market. What's less well known is just how dramatically that margin has changed over the past few decades. Competition, technology, and the rise of the betting exchange have collectively forced bookmakers to offer better and better odds — but only up to a point.

Read our What are the bookies margins on golf? article for a full explanation of how overrounds work.

What is an overround?

A fair betting market would see all the implied probabilities of each competitor sum to exactly 100%. In reality, bookmakers inflate those probabilities so the total exceeds 100% — that excess is the overround (also called the "vig", "juice", or "margin"). It represents the bookmaker's theoretical profit on every pound staked.

In golf, with fields of 100–156 players, overrounds are structurally much higher than in a two-runner market like a football match. There are simply more competitors to price — and more room to shave each player's odds slightly without any single price looking obviously wrong.

| Market type | Typical field size | Typical overround |

|---|---|---|

| Football match (1X2) | 3 outcomes | ~5–8% |

| Horse racing (handicap) | 8–16 runners | ~15–25% |

| Golf tournament outright | 100–156 players | ~25–50% |

The pre-internet era: when bookmakers called all the shots

Before the internet, betting was almost entirely conducted on the high street or at the track. The information asymmetry between bookmakers and punters was enormous: shops set their prices each morning and customers had no easy way to compare odds across firms. If William Hill offered 20/1 on a player and Coral offered 25/1, you wouldn't know unless you physically walked between branches.

This gave bookmakers enormous pricing power. On a golf tournament outright in the 1990s, it wasn't unusual to see overrounds well in excess of 100% — meaning the sum of implied probabilities across the entire field reached 200% or more. Punters weren't getting half the value they deserved and, crucially, had no practical way to know it.

The economics were simple: set every price slightly worse than fair value, and because no one could aggregate or compare, those margins were never arbitraged away.

| Era | Approx. golf outright overround | Context |

|---|---|---|

| Pre-internet (pre-2000) | 80–150%+ | No price comparison, no exchanges |

| Early online (2000–2008) | 50–90% | Competition begins, exchanges emerge |

| Competitive online (2009–2015) | 35–60% | Odds comparison sites, promotions war |

| Modern era (2016–present) | 25–55% | Tighter markets, but golf still high |

The Betfair effect: exchanges change everything

Betfair launched in June 2000 and quietly began one of the most significant disruptions in gambling history. Rather than betting against a bookmaker, punters could now bet against each other — and an efficient peer-to-peer market naturally finds fair odds far more accurately than any individual bookie.

The effect on traditional bookmakers was dramatic. Suddenly there was a reference price — a publicly available, efficient market price — against which any bookmaker's odds could be compared. Punters who previously had no way to know if they were getting value now had a benchmark.

Overrounds on football, horse racing, and tennis compressed rapidly as bookmakers were forced to compete. Golf was slower to respond — partly because exchanges need liquidity to work well, and a 156-man field is harder to trade than a two-team match — but the direction of travel was clear.

The arrival of odds comparison websites like OddsChecker (2001) accelerated this further. Bookmakers could no longer quietly offer poor value: every price was visible and comparable within seconds.

What our data shows: golf overrounds since 2016

![]() has been collecting odds data across PGA Tour and European Tour events since the beginning of 2016. Across that sample, the average overround has been a substantial 42.5% — meaning for every £100 worth of bets placed across the field, the bookmaker expects to pay out just £70.

has been collecting odds data across PGA Tour and European Tour events since the beginning of 2016. Across that sample, the average overround has been a substantial 42.5% — meaning for every £100 worth of bets placed across the field, the bookmaker expects to pay out just £70.

But averages hide a lot. The spread is wide, with a standard deviation of 7.0:

- 68% of events have an overround between 35.5% and 49.5%

- 95% of events have an overround between 28.5% and 56.5%

That upper tail — events approaching 55%+ — tends to be smaller, less prestigious tournaments where bookmakers face less sharp competition and feel less pressure to price accurately. The major championships (Masters, US Open, The Open, PGA Championship) consistently attract sharper markets and lower overrounds, often closer to 30–35%, because the volume of informed money is far higher.

Compare this to what the same bookmakers would have charged a decade earlier, and the improvement is real — but golf still lags behind other sports significantly. A Premier League match routinely sees overrounds of just 5–7%. Even a busy horse racing card rarely exceeds 20–25% per race.

| Tournament type | Typical overround (modern era) |

|---|---|

| Major championships | 28–36% |

| WGC / Signature events | 32–42% |

| Standard PGA / DP World Tour | 38–55% |

All events: overround over time

Each dot is one tournament. The green line is a 10-event moving average.

Majors only

The four majors attract sharper money — their overrounds are consistently lower.

Why golf overrounds are still so high

Despite decades of market compression, golf outrights remain one of the worst-value betting markets available. There are structural reasons for this:

- Large fields. With 100–156 players, each individual price can be marginally shortened without the error being obvious. Shaving just 0.3% off each player's implied probability across 150 runners adds 45% to the overround.

- Low-liquidity exchanges. Betfair's golf markets rarely attract enough money to force bookmakers' hands. Without a deep, efficient reference market, there's less pressure to price accurately.

- Casual bettors. Golf attracts a higher proportion of casual, recreational bettors than horse racing or football. These customers are less price-sensitive and less likely to shop around — which means bookmakers face less pressure to sharpen up.

- Complexity of pricing. Accurately pricing 156 players across four rounds of golf is genuinely hard. Bookmakers compensate for their uncertainty by widening margins, especially on longer-priced outsiders.

How to protect yourself as a bettor

The history of overrounds tells us one thing clearly: bookmakers price their markets in their favour, and golf is worse than almost any other sport. But that doesn't mean you can't win.

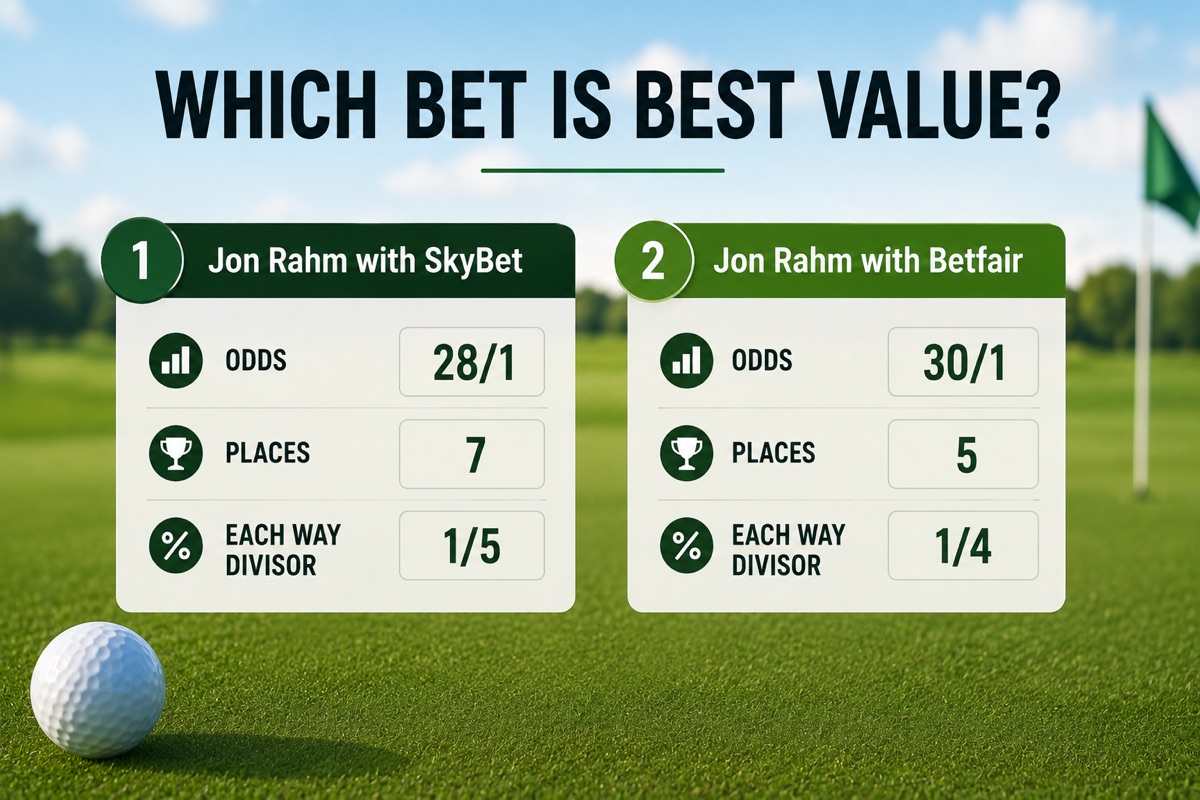

The key is to identify where within the overround the bookmaker has introduced the most error. In a 42.5% overround market, the bookmaker hasn't priced every player 42.5% worse than fair — they've distributed that margin unevenly. Short-priced favourites (which attract most of the money) tend to be priced more efficiently. Longer-priced players, particularly those in the 20/1–100/1 range, often carry disproportionately high margins because the bookmaker faces less scrutiny on those prices.

Finding value means identifying players the market has underestimated. That's exactly what ![]() is built to do — compare the bookmaker's implied probabilities against our model's predictions to surface the best-value bets each week.

is built to do — compare the bookmaker's implied probabilities against our model's predictions to surface the best-value bets each week.

See the Forecasts page to see where the value lies in this week's events.